26

Supervisory Insights Summer 2012

This regular feature focuses on

topics of critical importance to

bank accounting. Comments on

this column and suggestions for

future columns can be e-mailed to

Over the last several years, many

parts of the United States experienced

declining real estate values and high

rates of unemployment. This economic

environment has rendered some

borrowers unable to repay their debt

according to the original terms of their

loans. Interagency guidance encour-

ages bankers to work with borrowers

who may be facing financial difficul-

ties.

1

Prudent loan modifications are

often in the best interest of financial

institutions and borrowers, and in

fact many financial institutions are

restructuring or modifying loan terms

to provide payment relief for borrow-

ers whose financial condition has

deteriorated. These loan modifications

may meet the definition of a troubled

debt restructuring (TDR) found in the

accounting standards.

FDIC examiners and supervisors

frequently receive questions from

bankers about TDRs. Often the

answers to these questions can be

found in the framework for TDRs

established by the accounting stan-

dards, a framework which governs the

identification of TDRs, the impairment

analysis that banks must perform,

and the required disclosures. Other

important guidance is found in the

banking agencies’ published instruc-

tions for the Consolidated Reports of

Condition and Income (Call Report)

and selected policy statements of the

federal banking agencies. This article

summarizes and distills the aspects

of these standards and guidance that

are most relevant to identifying and

accounting for TDRs and complying

with the associated regulatory report-

ing requirements.

2

Accounting Guidance

A modification of the terms of a loan

is a TDR when a borrower is troubled

(i.e., experiencing financial difficul-

ties) and a financial institution grants

a concession to the borrower that it

would not otherwise consider. The

following discussion will focus on the

generally accepted accounting prin-

ciples (GAAP) that provide relevant

guidance for the financial reporting

of TDRs. The Financial Accounting

Standards Board’s (FASB) Accounting

Standards Codification (ASC) Topic

310 provides the basis for identifying

TDRs and treating TDRs as impaired

loans when estimating allocations

to the allowance for loan and lease

losses (ALLL).

3

In this regard, ASC

Accounting News:

Troubled Debt Restructurings

1

FIL-35-2007, Statement on Working with Mortgage Borrowers, April 17, 2007, www.fdic.gov/news/news/finan-

cial/2007/fil07035.html; FIL-128-2008, Interagency Statement on Meeting the Needs of Creditworthy Borrowers,

November 12, 2008, www.fdic.gov/news/news/financial/2008/fil08128.html; FIL-61-2009, Policy Statement on

Prudent Commercial Real Estate Loan Workouts, October 30, 2009, www.fdic.gov/news/news/financial/2009/

fil09061.html; and FIL-5-2010, Interagency Statement on Meeting the Credit Needs of Creditworthy Small Business

Borrowers, February 12, 2010, www.fdic.gov/news/news/financial/2010/fil10005.html.

2

Additional guidance on accounting for TDRs is included in the transcript from the FDIC’s Seminar on Commer-

cial Real Estate Loan Workouts and Related Accounting Issues, December 15, 2011, www.fdic.gov/news/

conferences/2011-12-15-transcript.html.

3

ASC Subtopic 310-40, Receivables – Troubled Debt Restructurings by Creditors (formerly Statement of Financial

Accounting Standards No. 15, Accounting by Debtors and Creditors for Troubled Debt Restructurings), and ASC

Subtopic 310-10, Receivables – Overall (formerly Statement of Financial Accounting Standards No. 114, Account-

ing by Creditors for Impairment of a Loan), respectively.

27

Supervisory Insights Summer 2012

Subtopic 310-40 addresses receiv-

ables that are TDRs from the lending

institution’s standpoint. Other GAAP

guidance addresses the accounting

for TDRs from the borrower’s stand-

point, a discussion of which is beyond

the scope of this article.

4

Finally, this

article incorporates the new guidance

in the FASB’s Accounting Standards

Update No. 2011-02 (ASU 2011-02)

that, among other clarifications of TDR

issues, discusses whether a delay in

payment as part of a loan modifica-

tion is insignificant.

5

These resources

along with complementary regulatory

guidance provide the foundation for

discussing TDRs.

Identification of a TDR

A TDR involves a troubled borrower

and a concession by the creditor. ASU

2011-02 identifies several indicators a

creditor must consider in determining

whether a borrower is experiencing

financial difficulties. These indica-

tors include, for example, whether

the borrower is currently in payment

default on any of its debt and whether

it is probable the borrower would be

in payment default on any debts in the

foreseeable future without the modifi-

cation. Thus, a borrower does not have

to be in payment default at the time

of the modification to be experienc-

ing financial difficulties. Types of loan

modifications that may be concessions

that result in a TDR include, but are

not limited to:

A reduction of the stated interest

rate for the remaining original life of

the debt,

An extension of the maturity date or

dates at a stated interest rate lower

than the current market rate for

new debt with similar risk,

A reduction of the face amount

or maturity amount of the debt as

stated in the instrument or other

agreement, or

A reduction of accrued interest.

The lending institution’s concession

to a troubled borrower may include

a restructuring of the loan terms to

alleviate the burden of the borrower’s

near-term cash requirements, such

as a modification of terms to reduce

or defer cash payments to help the

borrower attempt to improve its

financial condition. An institution

may restructure a loan to a borrower

experiencing financial difficulties at

a contractual interest rate below a

current market interest rate, which

normally is considered to be a conces-

sion resulting in a TDR. However, a

change in the interest rate on a loan

does not necessarily mean that the

modification is a TDR. For example,

an institution may lower the interest

rate to maintain a relationship with a

borrower that can readily obtain funds

from other sources. In this scenario,

extending or renewing the borrower’s

loan at the current market interest rate

for new debt with similar risk is not

a TDR. To be designated a TDR, both

borrower financial difficulties and a

lender concession must be present at

the time of restructuring.

Determining whether a modification

is at a current market rate of interest

at the time of the restructuring can be

challenging. The following scenarios

4

ASC Subtopic 470-60, Debt – Troubled Debt Restructurings by Debtors (formerly Statement of Financial Account-

ing Standards No. 15, Accounting by Debtors and Creditors for Troubled Debt Restructurings).

5

Accounting Standards Update No. 2011-02, A Creditor’s Determination of Whether a Restructuring Is a Troubled

Debt Restructuring.

28

Supervisory Insights Summer 2012

regarding interest rates on modified

loans are often encountered:

Rate for a troubled versus nontrou-

bled borrower – The stated interest

rate charged to a troubled borrower

in a loan restructuring may be

greater than or equal to interest

rates available in the marketplace

for similar types of new loans to

nontroubled borrowers at the time

of the restructuring. Some institu-

tions have concluded these restruc-

turings are not TDRs, which may

not be the case. These institutions

may not have considered all the

facts and circumstances – other

than the interest rate – associated

with the loan modification. An inter-

est rate on a modified loan greater

than or equal to those available in

the marketplace for similar new

loans to nontroubled borrowers does

not preclude a modification from

being designated as a TDR when the

borrower is troubled.

Market rate for a troubled borrower

– Generally, the contractual interest

rate on a modified loan is a current

market interest rate if the restruc-

turing agreement specifies an inter-

est rate greater than or equal to the

rate the institution was willing to

accept at the time of the restructur-

ing for a new loan with comparable

risk, i.e., comparable to the risk on

the modified loan. The contractual

interest rate on a modified loan is

not a market interest rate simply

because the interest rate charged

under the restructuring agreement

has not been reduced.

Below-market rate – According

to ASU 2011-02, if a borrower

does not have access to funds at

a market interest rate for debt

with similar risk characteristics as

the restructured debt, the rate on

the modified loan is considered a

below-market rate and may indi-

cate the institution has granted a

concession to the borrower.

Increased rate – When a modifica-

tion results in either a temporary or

permanent increase in the contrac-

tual interest rate, the increased

interest rate does not preclude the

modification from being considered

a concession. As noted in ASU 2011-

02, the new contractual rate on the

modified loan could still be a below

market interest rate for new debt

with similar risk characteristics.

When evaluating a loan modification

to a borrower experiencing finan-

cial difficulties, all relevant facts and

circumstances must be considered in

determining whether the institution

has made a concession to the troubled

borrower with respect to the market

interest rate or has made some other

type of concession that could trigger

TDR accounting and disclosure. This

determination requires the use of judg-

ment and should include an analysis of

credit history and scores, loan-to-value

ratios or other collateral protection,

the borrower’s ability to generate cash

flow sufficient to meet the repayment

terms, and other factors normally

considered when underwriting and

pricing loans. If the terms or condi-

tions related to a restructured loan

to a borrower experiencing financial

difficulties are outside the institution’s

policies or common market practices,

then the restructuring may be a TDR.

Financial institutions must exercise

judgment and carefully document their

conclusions about market interest rates

and other terms and conditions under

restructuring agreements and whether

the restructurings are TDRs.

A modification of a loan to a borrower

experiencing financial difficulties

involving only a delay in payment also

needs to be evaluated for TDR status.

According to ASU 2011-02, lenders

Troubled Debt Restructurings

continued from pg. 27

29

Supervisory Insights Summer 2012

must consider many factors, including,

but not limited to the following:

the amount of the delayed

payments in relation to the loan’s

unpaid principal or collateral value,

the frequency of payments due on

the loan,

the original contractual maturity of

the loan, and

the original expected duration of the

loan.

If an institution determines that a

restructuring results in only a delay in

payment that is insignificant, then the

institution has not granted a conces-

sion to the borrower. This determina-

tion may lead to the conclusion that a

particular modification to a troubled

borrower is not a TDR.

Impairment

All held-for-investment loans

whose terms have been modified in

a TDR are impaired loans that must

be measured for impairment under

ASC Subtopic 310-10. This guid-

ance applies even if the loan that has

undergone a TDR is not otherwise

individually evaluated for impairment

under ASC Subtopic 310-10, as in

the case of residential mortgages and

other smaller-balance homogeneous

loans that are collectively evaluated

for impairment. ASC Subtopic 310-10

specifies that an institution should

measure impairment (and, hence, the

amount of any allocation to the ALLL

for an impaired loan) based on:

the present value of expected future

cash flows discounted at the loan’s

effective interest rate,

the loan’s observable market price,

or

the fair value of the collateral if the

loan is collateral dependent.

The fair value of collateral and pres-

ent value of expected future cash flows

methods warrant further discussion.

When an impaired loan is collateral

dependent, the banking agencies’

regulatory reporting guidance requires

that the fair value of collateral method

be used to measure impairment.

6

In

contrast, the fair value of collateral

method may not be used when an

impaired loan is not collateral depen-

dent, even if the loan is collateralized.

An impaired loan, including a TDR,

is collateral dependent if repayment

of the loan is expected to be provided

solely by the underlying collateral and

there are no other available and reli-

able sources of repayment. Accord-

ing to ASC Subtopic 310-10, if an

institution uses the fair value of the

collateral to measure impairment of

an impaired collateral dependent loan,

and repayment or satisfaction of the

loan is dependent only on the opera-

tion, rather than the sale, of the collat-

eral, estimated costs to sell should not

be incorporated into the impairment

measurement. In contrast, an institu-

tion should adjust the fair value of the

collateral to consider estimated costs to

sell when measuring the impairment of

an impaired collateral dependent loan

if repayment or satisfaction of the loan

is dependent on the sale of the collat-

eral. According to the December 2006

Interagency Policy Statement on the

Allowance for Loan and Lease Losses,

any portion of the recorded investment

in an impaired collateral dependent

loan in excess of the fair value of the

collateral (less estimated costs to sell,

if appropriate) that can be identified

as uncollectible (i.e., a confirmed loss)

should be promptly charged off against

6

GAAP permits impairment on an impaired collateral dependent loan to be measured based on the fair value of

the collateral, but requires the use of this impairment measurement method only when foreclosure is probable.

30

Supervisory Insights Summer 2012

7

FIL-105-2006, Allowance for Loan and Lease Losses Revised Policy Statement and Frequently Asked Questions,

December 13, 2006, www.fdic.gov/news/news/financial/2006/fil06105.html.

8

Ibid.

9

Instructions for the Preparation of Consolidated Reports of Condition and Income, Glossary, “Allowance

for Loan and Lease Losses,” page A-3 (9-10), http://www.fdic.gov/regulations/resources/call/crinst/2012-

03/312Gloss_033112.pdf.

10

Furthermore, the Uniform Retail Credit Classification and Account Management Policy calls for charge-offs of

retail loans, including TDRs, in certain circumstances. See FIL-40-2000, June 29, 2000, www.fdic.gov/news/news/

financial/2000/fil0040.html.

Troubled Debt Restructurings

continued from pg. 29

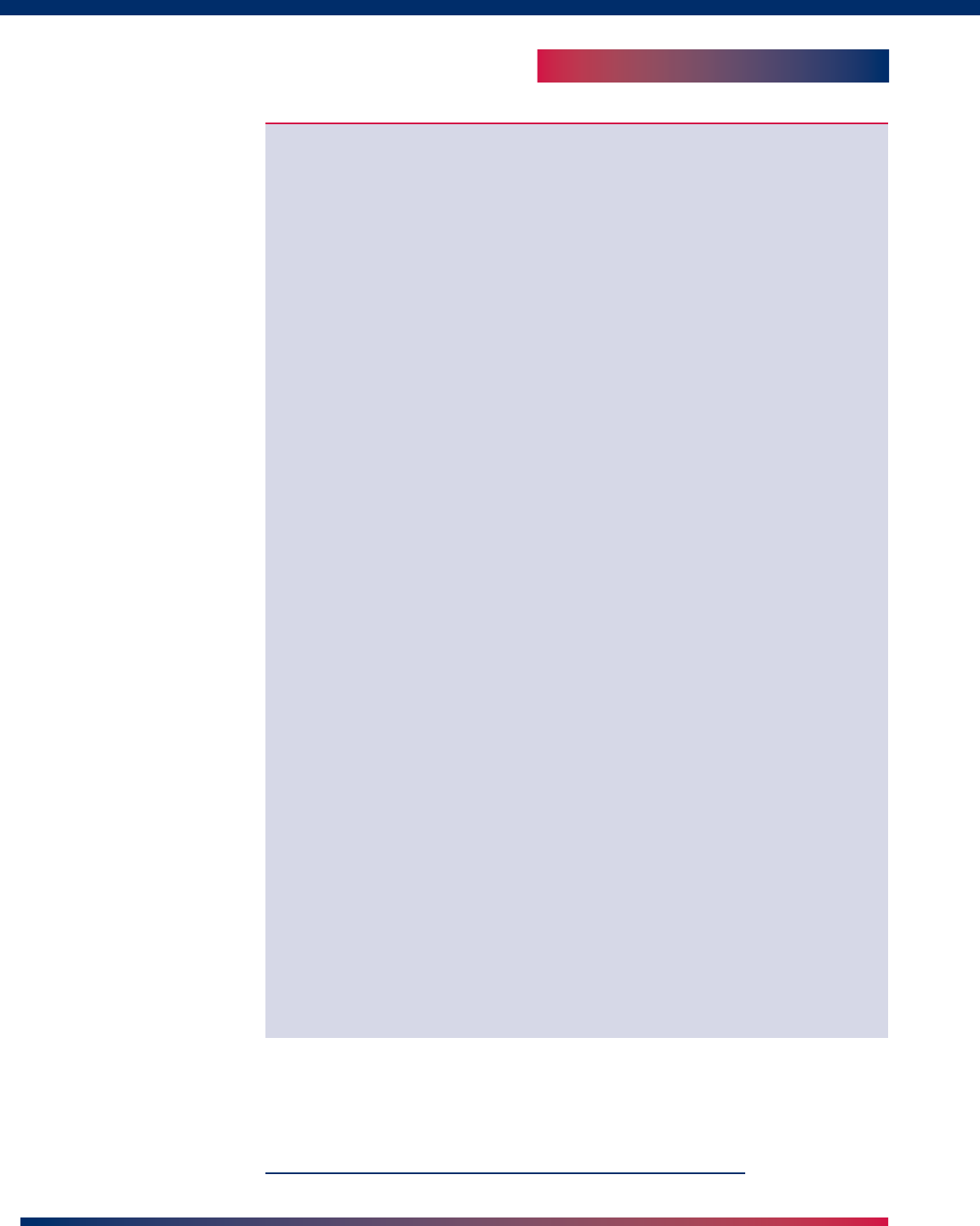

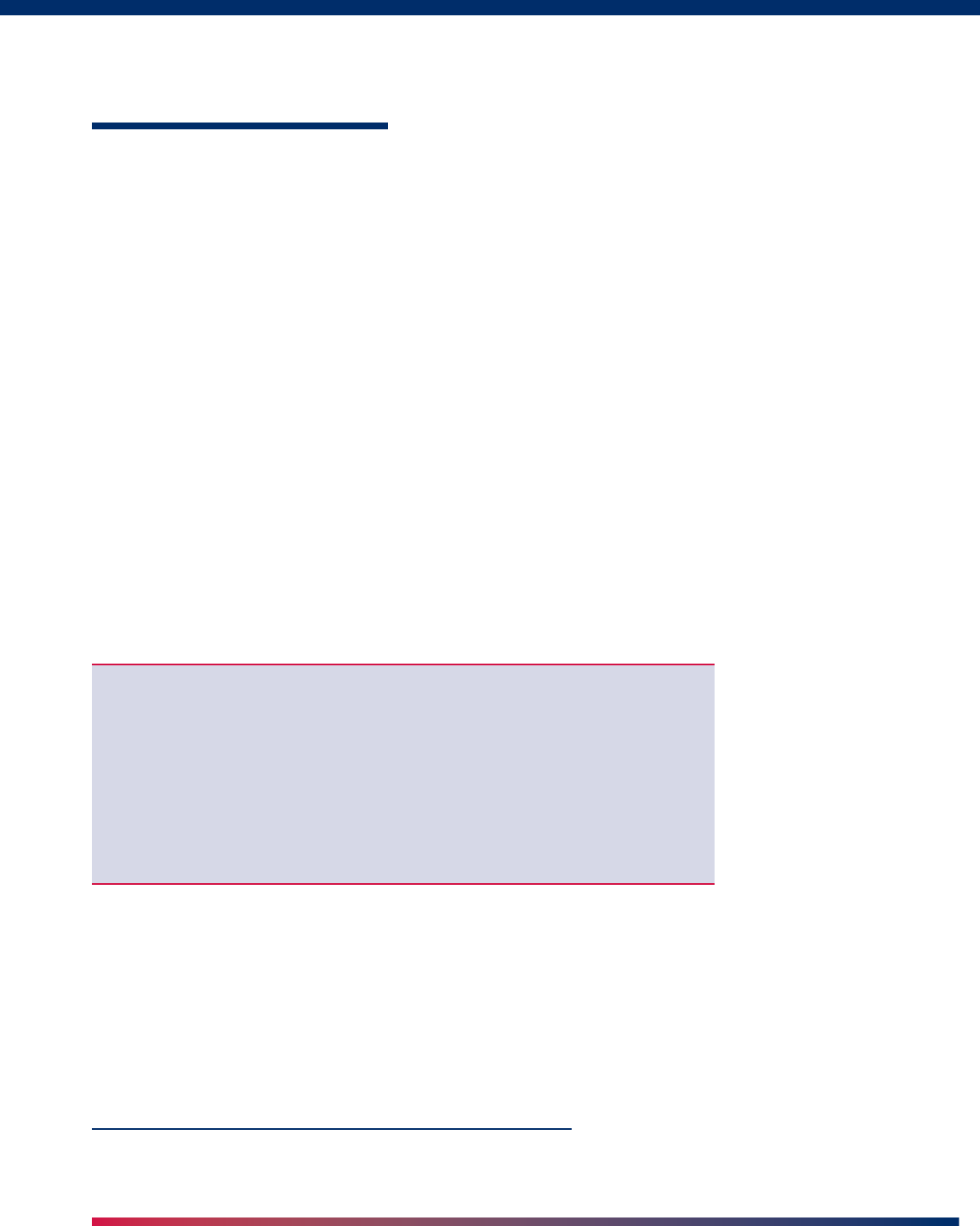

Fair Value of Collateral Method

Questions and Answers

Q) Is the definition of collateral dependent for regulatory reporting purposes the same

as under GAAP, which includes loans for which the cash flow from the operation of the

collateral is the only source of repayment? Or is a loan collateral dependent only when

repayment is dependent on the sale of the collateral?

A) Collateral dependent is defined in ASC Subtopic 310-10, which is the same definition

used in the December 2006 Interagency Policy Statement on the Allowance for Loan

and Lease Losses: A loan is collateral dependent if repayment of the loan is expected

to be provided solely by the underlying collateral.

7

The instructions for the Call Report

elaborate on this definition, noting that it applies to situations where there are no other

available and reliable sources of repayment other than the underlying collateral. Thus,

the definition of collateral dependent includes cases where repayment of the loan is

dependent on the sale of the collateral as well as cases where repayment is dependent

only on the operation of the collateral.

Q) Impairment measurement on an impaired collateral dependent loan for which repay-

ment is dependent only on the operation of the collateral should not reflect costs to sell.

What is the reference for this guidance?

A) FASB Statement No. 114, Accounting by Creditors for Impairment of a Loan, was the

original source. This guidance is now in ASC paragraph 310-10-35-23, which states “if

repayment or satisfaction of the loan is dependent only on the operation, rather than the

sale, of the collateral, the measure of impairment shall not incorporate estimated costs to

sell the collateral.”

Q) When is an allocation to the ALLL appropriate for a collateral dependent TDR and when

is a charge-off needed?

A) The December 2006 Interagency Policy Statement on the Allowance for Loan and

Lease Losses and the Glossary section of the Call Report instructions provide guidance

on measuring impairment relevant to TDRs. Each institution must maintain an ALLL at a

level appropriate to cover estimated credit losses associated with the loan and lease

portfolio in accordance with GAAP.

8

Additions to, or reductions of, the ALLL are to be

made through charges or credits to the “provision for loan and lease losses” in the Call

Report income statement.

9

When available information confirms that specific loans or

portions thereof are uncollectible, including loans that are TDRs, these amounts should be

promptly charged off against the ALLL.

10

31

Supervisory Insights Summer 2012

the ALLL.

12

Institutions must apply the

fair value of collateral method appro-

priately to TDRs.

With regard to the present value of

cash flows method, an institution’s esti-

mate of the expected future cash flows

on a TDR should be its best estimate

based on reasonable and supportable

assumptions (including default and

prepayment assumptions) and projec-

tions. GAAP also specifies the effective

interest rate to be used for discount-

ing. Under ASC Subtopic 310-10, when

measuring impairment on a TDR using

the present value of expected future

cash flows method, the cash flows

should be discounted at the effective

interest rate of the original loan, not

the rate after the restructuring. For

a restructured residential mortgage

loan that originally had a “teaser” or

starter rate less than the loan’s fully

indexed rate, the starter rate is not the

original effective interest rate. In this

case, the effective interest rate should

be a blend of the “teaser” rate and the

fully indexed rate. If the results are

not materially different from using the

blended rate, the fully indexed rate

may be used as the effective interest

rate. Using the proper effective inter-

est rate is critical to allocating the

appropriate amount to the ALLL when

measuring impairment on a TDR under

the present value method.

11

FIL-61-2009, Policy Statement on Prudent Commercial Real Estate Loan Workouts, October 30, 2009, www.fdic.

gov/news/news/financial/2009/fil09061.html.

12

FIL-105-2006, Allowance for Loan and Lease Losses Revised Policy Statement and Frequently Asked Questions,

December 13, 2006, www.fdic.gov/news/news/financial/2006/fil06105.html.

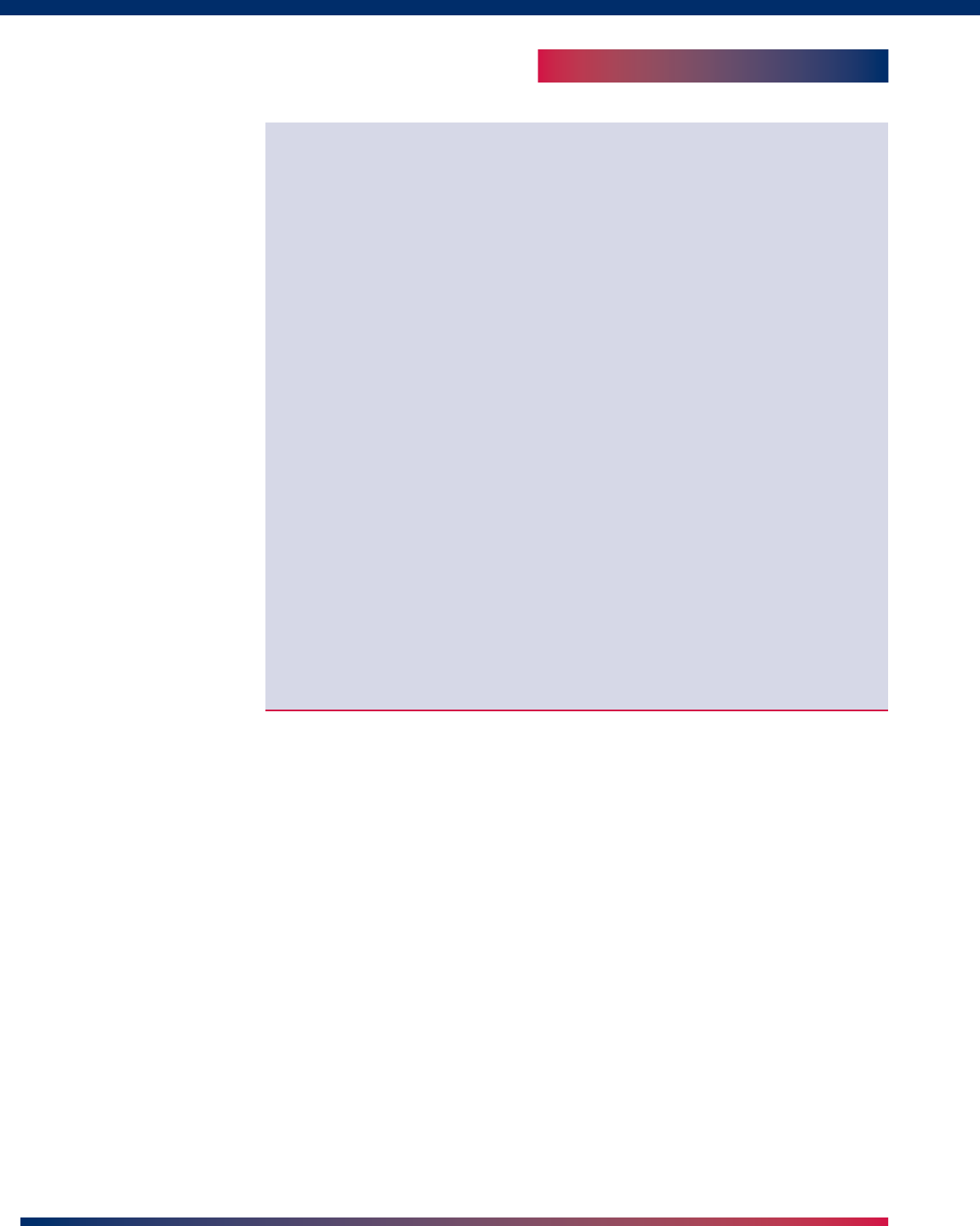

For an individually evaluated impaired collateral dependent loan, including a TDR, the

banking agencies require that impairment be measured using the fair value of collateral

method in ASC Subtopic 310-10. In this situation, as discussed in the October 2009 Policy

Statement on Prudent Commercial Real Estate Loan Workouts, if the recorded amount of

the loan exceeds the fair value of the collateral (less costs to sell if repayment of the loan

is dependent on the sale of the collateral), this excess represents the measurement of

impairment on the loan and is the amount to be included for this loan in the overall ALLL.

However, determining the portion of this difference that represents a confirmed loss, if

any, which should be charged against the ALLL in a timely manner, is based on whether

repayment is dependent on the sale or only on the operation of the collateral.

11

Q) Are institutions required to evaluate impairment using the present value of expected

future cash flows method when an impaired loan, including a TDR, is not collateral depen-

dent? Can an institution use the fair value of collateral method to measure impairment on

an impaired non-collateral dependent loan?

A) A TDR is not collateral dependent when there are available and reliable sources of

repayment other than the sale or operation of the collateral. ASC Subtopic 310-10 acknowl-

edges that a loan’s observable market price may be used as a practical expedient to

measure impairment. However, such a price is not usually available for individual impaired

loans, including TDRs. Therefore, the present value of expected future cash flows method

normally would be used when a TDR is not collateral dependent.

The fair value of collateral method may only be used when an impaired loan, including a

TDR, is collateral dependent. It would be inappropriate under GAAP to measure impair-

ment using the fair value of collateral method when an impaired loan or TDR is not

collateral dependent.

32

Supervisory Insights Summer 2012

Applying the Appropriate Impairment Measurement Method

Example 1: Discounted Cash Flow Method

FACTS: A banker makes a commercial loan to a small wholesale business, which has a

market interest rate at origination. The loan matures in five years and is secured by a first

lien on the business’s warehouse.

After 24 months, the local economy has weakened, adversely affecting the borrower’s

wholesale business. The borrower has fallen delinquent on several loans including this

commercial loan, which is 90 days past due. After carefully analyzing the borrower’s

personal and business financial statements and credit reports, the banker determines

that it is likely the borrower’s business will be able to generate only enough cash flow

to partially service this commercial loan. The borrower plans to operate the business

for five more years and expects economic conditions to improve by the end of this

period, enabling the borrower to sell the business at that time, including remaining

inventory and the warehouse.

The banker decides to restructure the remaining principal balance of this commercial

loan to mature in five years. Based on the borrower’s expected cash flows from the

business, the banker lowers the contractual interest rate to a below market rate (i.e.,

to an interest rate that is less than the rate the banker would charge at the time of the

restructuring for a new loan with comparable risk). The required monthly payments are

reduced, with these payments expected to come from business operations. A balloon

payment is scheduled at the end of five years.

Based on reasonable and supportable assumptions and projections, which take default

probability into account, the banker develops an estimate of the expected monthly

cash flows over the five year loan term. The banker also concludes that the current

“as is” appraised value of the warehouse is not likely to increase over this period.

Considering the borrower’s current inventory levels and other information, the banker

estimates that the sale of the borrower’s warehouse and other available business

assets at the end of five years would generate additional funds to satisfy the debt.

Considering all available evidence, including the borrower’s current financial difficul-

ties, the banker’s best estimate is that 90 percent of the contractual loan payments

under the modified terms will be collected.

IMPAIRMENT MEASUREMENT METHOD: This restructured commercial loan is a TDR

subject to impairment measurement in accordance with ASC Subtopic 310-10. Because

the available and reliable sources of repayment include cash flow from the borrower’s

business operations, this commercial loan is not collateral dependent. The banker will use

the discounted cash flow method to determine the impairment amount.

13

13

The commercial loan does not have an observable market price.

Troubled Debt Restructurings

continued from pg. 31

33

Supervisory Insights Summer 2012

Example 2: Fair Value of Collateral Method

FACTS: A banker makes a commercial real estate loan, the collateral for which is an

apartment building. The collateral at origination has normal occupancy and rental rates

and its value provides sufficient collateral coverage.

The borrower subsequently experiences financial difficulties. The banker obtains a

current appraisal, which shows that the prospective “as stabilized” and the “as is”

market values have declined in comparison to market values in the original appraisal

as a result of a significantly increased vacancy rate and a decline in rental rates. The

banker has reviewed the current appraisal and found the assumptions and conclusions

to be reasonable.

The banker also concludes that the current “as is” market value conclusion is an

appropriate estimate of the fair value of the collateral for financial reporting purposes.

Available evidence indicates that the local economy is beginning to improve. Thus,

the banker reasonably expects that the property will reach the current appraisal’s

prospective “as stabilized” value within two years.

The borrower has no other assets and his ability to service the debt from other sources

is nonexistent.

After a thorough analysis of the borrower’s financial condition and the operating

statements for the apartment building, the banker concludes that the loan can be

repaid only through the operation of the collateral. Liquidation of the collateral is not

anticipated.

The banker determines that a prudent loan workout would be in the best interest of

the bank and the borrower. In order to recover as much of the loan as reasonably

possible, the banker negotiates reduced monthly payments that the cash flow from the

apartment building is expected to be sufficient to service at an interest rate below a

current market interest rate for a new loan with comparable risk.

IMPAIRMENT MEASUREMENT METHOD: This restructured commercial real estate loan is

a TDR subject to impairment measurement in accordance with ASC Subtopic 310-10. This

commercial real estate loan is collateral dependent. The banker must use the fair value of

collateral method to determine the impairment amount. Only the operation of the collateral

is expected to repay this loan; therefore, the measurement of impairment shall not incor-

porate estimated costs to sell the collateral.

34

Supervisory Insights Summer 2012

Example 3: Fair Value of Collateral Method

FACTS: Same as Example 2 except that a thorough analysis of the borrower’s financial

condition, the operating statements for the apartment building, and the borrower’s inabil-

ity to increase rental rates, leads the banker to conclude that the apartment building

provides insufficient collateral coverage. Local economic conditions are not expected to

improve in the near term and the banker is not confident that the current appraisal’s “as

stabilized” market value can be achieved within a reasonable time period.

As a consequence, the banker determines that repayment of the loan is dependent

on the liquidation of the collateral by the borrower or by the bank through foreclo-

sure. As an interim measure to recognize the apartment building’s reduced cash flow

until collateral liquidation, the banker modifies the loan terms to lower the monthly

payments at an interest rate below a current market interest rate for a new loan with

comparable risk.

Under either scenario, the banker has determined that the well supported current

appraisal’s “as is” market value conclusion is an appropriate estimate of the fair value

of the collateral.

Costs to sell the property are estimated.

IMPAIRMENT MEASUREMENT METHOD: This restructured commercial real estate loan is

a TDR subject to impairment measurement in accordance with ASC Subtopic 310-10. This

commercial real estate loan is collateral dependent. The banker must use the fair value

of collateral method to determine the impairment amount. Liquidation of the collateral is

expected to repay this loan; therefore, the measurement of impairment must incorporate

estimated costs to sell the collateral.

The appropriate impairment measure-

ment method, determined as

discussed above, is applied to TDRs

and other impaired loans on a loan-

by-loan basis. However, ASC Subtopic

310-10 permits an institution to aggre-

gate impaired loans that share risk

characteristics in common with other

impaired loans. For example, modified

residential mortgage loans that repre-

sent TDRs and have common risk

characteristics may be aggregated for

impairment measurement purposes.

In this scenario, an institution uses

historical statistics along with a

composite effective interest rate to

measure impairment of this pool

of impaired loans. Institutions may

aggregate TDRs to measure impair-

ment in accordance with GAAP and

regulatory guidance.

Troubled Debt Restructurings

continued from pg. 33

35

Supervisory Insights Summer 2012

Accrual Status

The Glossary section of the Call

Report instructions provides guid-

ance for nonaccrual status, which is

consistent with GAAP and applies to

loans that have undergone TDRs. The

general rule is that institutions shall

not accrue interest on any loan:

which is maintained on a cash basis

because of deterioration in the

financial condition of the borrower,

for which payment in full of princi-

pal or interest is not expected, or

upon which principal or interest has

been in default for a period of 90

days or more unless the loan is both

“well secured” and “in the process

of collection.”

14

Assuming the accrual of interest

has not already been discontinued on

a loan undergoing a TDR, this Call

Report general rule should be consid-

ered when evaluating whether the loan

should be placed in nonaccrual status.

However, the general rule need not

be applied to consumer loans and

loans secured by one-to-four family

residential properties on which prin-

cipal or interest is due and unpaid

for at least 90 days. If not placed in

nonaccrual status, these loans should

be subject to alternative methods

of evaluation to assure the institu-

tion’s net income is not materially

overstated. When such consumer

and residential loans are treated as

nonaccrual by the institution, these

loans must be reported as nonaccrual

in the Call Report. The exception

from the general rule for nonaccrual

status and related guidance also apply

to consumer and residential loans

that are TDRs.

14

Instructions for the Preparation of Consolidated Reports of Condition and Income, Glossary, “Nonaccrual

Status,” page A-59 (9-10), http://www.fdic.gov/regulations/resources/call/crinst/2012-03/312Gloss_033112.pdf.

15

Ibid.

A loan is “well secured” if it is secured by collateral in the form of liens on or pledges

of real or personal property, including securities, with a realizable value sufficient to

discharge the debt (including accrued interest) in full, or by the guarantee of a finan-

cially responsible party.

A loan is “in the process of collection” if collection of the loan is proceeding in due

course through either legal action or other collection efforts which are reasonably

expected to result in repayment of the loan or in its restoration to a current status in

the near future.

15

36

Supervisory Insights Summer 2012

A nonaccrual loan may be restored

to accrual status:

when none of its principal and

interest is due and unpaid, and the

institution expects repayment of the

remaining contractual principal and

interest, or

when it becomes “well secured”

and “in the process of collection” as

previously defined.

With regard to satisfying the first

parameter, the institution must have

received repayment of the past-due

principal and interest unless the loan

has been formally restructured in a

TDR and qualifies for accrual status.

Thus, a nonaccrual loan that has been

formally restructured and is reason-

ably assured of repayment (of prin-

cipal and interest) and performance

according to the modified terms may

be returned to accrual status even

though amounts past due under the

original contractual terms have not

been repaid. In this scenario, the

restructuring and any charge-off taken

on the loan must be supported by

a current, well documented credit

evaluation of the borrower’s financial

condition and prospects for repay-

ment under the modified terms.

Otherwise, the restructured loan must

remain in nonaccrual status. The

credit evaluation must include consid-

eration of the borrower’s sustained

historical repayment performance

for a reasonable period before the

date the loan is returned to accrual

status. A sustained period of repay-

ment performance is generally a

minimum of six months and involves

payments of cash or cash equivalents.

In returning a nonaccrual TDR to

accrual status, sustained historical

repayment performance for a reason-

able time before the restructuring may

be considered. Such a restructuring

must improve the collectability of the

loan in accordance with a reason-

able repayment schedule and does

not relieve the institution from the

responsibility to promptly charge off

identified losses. Returning a nonac-

crual TDR to accrual status must be

carefully documented and supported.

The structure of a modified loan

that is a TDR may influence whether

the loan is reported in nonaccrual

or accrual status. A formal restruc-

turing may involve a multiple note

structure in which a troubled loan is

divided into two notes. In accordance

with the October 2009 Policy State-

ment on Prudent Commercial Real

Estate Loan Workouts

16

and the Call

Report instructions, institutions may

separate the portion of an outstand-

ing troubled loan into a new legally

enforceable note (i.e., the first note)

that is reasonably assured of repay-

ment (of principal and interest) and

performance according to prudently

modified terms. The second note

represents the portion of the original

loan that is unlikely to be collected

and has been charged off at or before

the restructuring. The first note may

be placed in accrual status provided

the conditions in the preceding para-

graph are met and the restructuring

has economic substance and qualifies

as a TDR under GAAP.

In contrast, a loan that undergoes

a TDR should remain or be placed

in nonaccrual status if the modifica-

tion does not include the splitting of

the troubled loan into multiple notes,

but the institution instead internally

16

FIL-61-2009, Policy Statement on Prudent Commercial Real Estate Loan Workouts, October 30, 2009, www.fdic.

gov/news/news/financial/2009/fil09061.html.

Troubled Debt Restructurings

continued from pg. 35

37

Supervisory Insights Summer 2012

recognizes a partial charge-off for the

identified loss on the loan before or

at the time of its restructuring as a

single note. A partial charge-off would

indicate the institution does not

expect full repayment of the amounts

contractually due under the loan’s

original terms. After the restructuring,

the remaining balance of the TDR may

be returned to accrual status without

having to first recover the charged-off

amount if the conditions for returning

a nonaccrual TDR to accrual status

discussed above are met. The charged-

off amount may not be reversed or

re-booked when the loan is returned

to accrual status.

If a loan appropriately in accrual

status has its terms modified in a

TDR, the loan may not meet the crite-

ria for placement in nonaccrual status

at the time of the restructuring. The

TDR can remain in accrual status

provided the borrower’s sustained

historical repayment performance for

a reasonable time prior to the TDR

(generally a minimum of six months)

is consistent with the loan’s modi-

fied terms and the loan is reasonably

assured of repayment (of principal

and interest) and of performance in

accordance with its modified terms.

This determination must be supported

by a current, well documented credit

evaluation of the borrower’s financial

condition and prospects for repay-

ment under the revised terms.

Income on nonaccrual TDRs should

be reported in accordance with the

Call Report instructions and GAAP.

For a nonaccrual TDR, some or all of

the cash interest payments received

may be recognized as interest income

on a cash basis provided the remain-

ing recorded investment in the

loan (i.e., after charge-off of identi-

fied losses, if any) is deemed fully

collectible. If a nonaccrual TDR that

has been returned to accrual status

subsequently meets the criteria for

placement in nonaccrual status as a

result of past-due payments based on

its modified terms or for any other

reason, the TDR must again be placed

in nonaccrual status.

Regulatory Reporting

Properly applying the accounting

and Call Report requirements for

TDRs provides useful financial infor-

mation about the quality of the loan

portfolio and an institution’s efforts

to work with troubled borrowers. Two

Call Report schedules specifically

disclose information on TDRs by loan

category:

Schedule RC-C, Part I, “Loans and

Leases,” Memorandum item 1, if the

TDR is in compliance with its modi-

fied terms, and

Schedule RC-N, “Past Due and

Nonaccrual Loans, Leases, and

Other Assets,” Memorandum item 1,

if the TDR is not in compliance with

its modified terms.

To be considered in compliance

with its modified terms, a loan that is

a TDR must be in accrual status and

must be current or less than 30days

past due on its contractual princi-

pal and interest payments under the

modified terms. A TDR that meets

these conditions must be reported as

a restructured loan in Schedule RC-C,

Part I, Memorandum item 1. In the

calendar year after the year in which

38

Supervisory Insights Summer 2012

the restructuring took place a TDR

may be removed from being reported

in this memorandum item if:

the TDR is in compliance with its

modified terms, and

the restructuring agreement speci-

fies an interest rate that at the time

of the restructuring is greater than

or equal to the rate that the bank

was willing to accept for a new loan

with comparable risk, i.e., a market

interest rate.

17

When a loan has been restructured

in a TDR, it continues to be consid-

ered a TDR for purposes of measuring

impairment until paid in full or other-

wise settled, sold, or charged off, even

if disclosure of the loan as a TDR is no

longer required. The loan remains an

impaired loan for accounting purposes

because impairment is evaluated in

relation to the contractual terms spec-

ified by the original loan agreement,

not the restructured terms. Thus, the

impairment measurement require-

ments for impaired loans in ASC

Subtopic 310-10, discussed above,

continue to be applicable for all TDRs,

even if they are no longer subject to

disclosure as TDRs.

Conclusion

Regulators support institutions

proactively working with borrowers

in the current economic environment

to restructure loans with reasonable

modified terms and expect these

modifications to be properly reflected

in Call Reports. Although borrowers

may experience deterioration in their

financial condition and other chal-

lenges, many continue to be credit-

worthy customers with the willingness

and capacity to repay their debts.

In such cases, financial institutions

and borrowers may find it mutually

beneficial to work together to improve

the borrower’s repayment prospects.

Accurate Call Reports allow regulators

and the public to monitor the extent

and status of modifications that repre-

sent TDRs.

Shannon M. Beattie, CPA

Regional Accountant, New

York Region

The author acknowledges the valu-

able contributions of Robert F. Storch,

CPA, Chief Accountant and Robert B.

Coleman, CPA, Regional Accountant

to the writing of this article.

Troubled Debt Restructurings

continued from pg. 37

17

Instructions for the Preparation of Consolidated Reports of Condition and Income, Schedule RC-C, PartI, “Loans

and Leases,” page RC-C-21 (3-11), www.fdic.gov/regulations/resources/call/crinst/2011-09/911RC-C1_093011.pdf.