MBMA

INSURANCE

BULLETIN

no.

15

... look at the

basic insurance

costs of metal

buildings

compared to

other types

of building

construction.

© 2015 MBMA

HOW METAL BUILDING

INSURANCE COSTS COMPARE

TO OTHER BUILDING TYPES

Contractors who build with other products will compete with

metal buildings based on an assumption that insurance costs

are lower for their form of construction. While this can be

true, it can also be false. Understanding the information in the

various MBMA Insurance Bulletins, as well as the information

in the MBMA Insurance Facts document, will help you clarify

insurance cost, as well as overcome this potential issue in the

eyes of the customer.

In this bulletin we will take a look at the basic insurance

costs of metal buildings compared to other types of building

construction. In the example that follows, we will look at a

typical building that is 12,500 square feet and houses a pump

distribution warehouse and ofces. The building is described

in detail in the attached Property Narrative report that would

typically be developed by an insurance loss control specialist

to assist the underwriter in determining an insurance price.

While occupancy can impact insurance pricing (as described

in MBMA’s Insurance Bulletin No. 7), we will keep occupancy

(pump distribution warehouse) the same for all examples.

As stated in Insurance Facts, construction type is a primary

driver of insurance rates for buildings. The Insurance Services

Ofce (ISO) is the organization supported by the insurance

industry that compiles data used in developing insurance rates.

For rating purposes, ISO categorizes buildings into six classes:

FRAME (Construction Class 1)

These are buildings with exterior walls, oors, and roof of

combustible construction, or buildings with exterior walls of

noncombustible or slow-burning construction with combustible

oors and roof. Also included are buildings with walls and roofs

with composite assemblies which include both combustible

and noncombustible materials.

JOISTED MASONRY (Construction Class 2)

These are buildings with exterior walls of re-resistive

construction rated at not less than 1 hour, or of masonry with

combustible oors and roof.

NONCOMBUSTIBLE (Construction Class 3)

These are buildings with exterior walls, oors, and roof of

noncombustible or slow-burning materials supported by

noncombustible or slow-burning supports. Metal buildings

normally fall into this category.

MASONRY NONCOMBUSTIBLE (Construction Class 4)

These are buildings with exterior walls of re-resistive

construction rated at not less than 1 hour or masonry (not less

than 4” thick) and with noncombustible or slow-burning oors

and roof.

MODIFIED FIRE-RESISTIVE (Construction Class 5)

These are buildings with exterior walls, oors, and a roof

constructed of materials described in Construction Class 6 re-

resistive, but have a deciency in thickness and a re resistance

rating of less than 2 hours, but not less than 1 hour.

FIRE-RESISTIVE (Construction Class 6)

These are buildings with solid (not less than 4” thick) or hollow

(not less than 8” thick) masonry walls or assemblies with a re

resistance rating of not less than 2 hours and oor and roof

assemblies with re resistance rating of not less than 2 hours.

Horizontal and vertical load bearing protected metal supports,

with re resistance rating of not less than 2 hours, including

pre-stressed or post-tensioned concrete units.

In this example, our building is less than 15,000 square feet

so insurance pricing is typically based on building class rates

developed by the ISO as described in Insurance Bulletin No.

4. Buildings larger than 15,000 square feet are generally rated

individually by insurance companies, applying credits and

charges based on building and occupancy characteristics.

Loss Costs are the calculated loss per $100 of insured building

value and are generated by ISO from their database of

premiums and losses.

ISO calculates these by state and within regions of each state

using the historic losses reported to them by all insurance

companies. Most states have adopted ISO Loss Cost

calculations as a basis for re insurance rates in the state.

Losses are aggregated on a state-by-state basis by ISO and

are also aggregated by specic areas within a state when

environmental factors such as high winds or earthquakes are

prevalent. ISO also aggregates losses by building type. These

historic losses are then published for states and insurers to use

in the development of their specic rates. As a result, all states

© 2015 MBMA

... insurance pricing

is typically based on

building class rates

developed by the

ISO as described in

Insurance Bulletin

No. 4...

and insurance carriers using ISO Loss Cost data start with the

same basic information.

Most insurance carriers use the ISO-developed Loss Costs to

calculate the rates they charge.

Each carrier multiplies the ISO-developed Loss Cost rate by

their own loss conversion factor or LCF. LCF’s are led by each

insurance carrier in each state. States vary in procedure, but

they either afrmatively approve the carrier’s LCF or accept it

as led. The LCF includes the insurance carrier’s cost of doing

business and also anticipates a margin of prot. In general,

these LCF’s range between 1.2 and 1.4. What you need to

remember is that, while the underlying ISO rate is uniform

across insurance carriers, the unique LCF for each carrier can

result in a range of prices. When comparing insurance costs

between metal buildings and other competitive types of

building construction, it is important to make sure the premium

pricing used is from the same insurance carrier.

The last variable in the cost of insurance is the actual value

of the building. All ISO rates and the LCF’s used to develop

pricing result in a dollar rate for each $100 of building value.

Let’s take a look at how these variables impact the cost of

insurance on our model building.

In a study completed in 2010, we looked at insuring our model

building in four different states. We also looked at insurance

costs if the model building were constructed in each of the six

ISO building classes. In addition, we compared the insurance

cost for each building type constructed in four different states

with differing environmental exposures.

As noted in the attached report, the four cities where the

model building was priced were:

Bryan, TX 77803

Delray Beach, FL 34444

DuBois, PA 15801

La Mesa, CA 91945

We assumed that, in each state, our hypothetical insurance

carrier had led a loss conversion factor of 1.4.

© 2015 MBMA

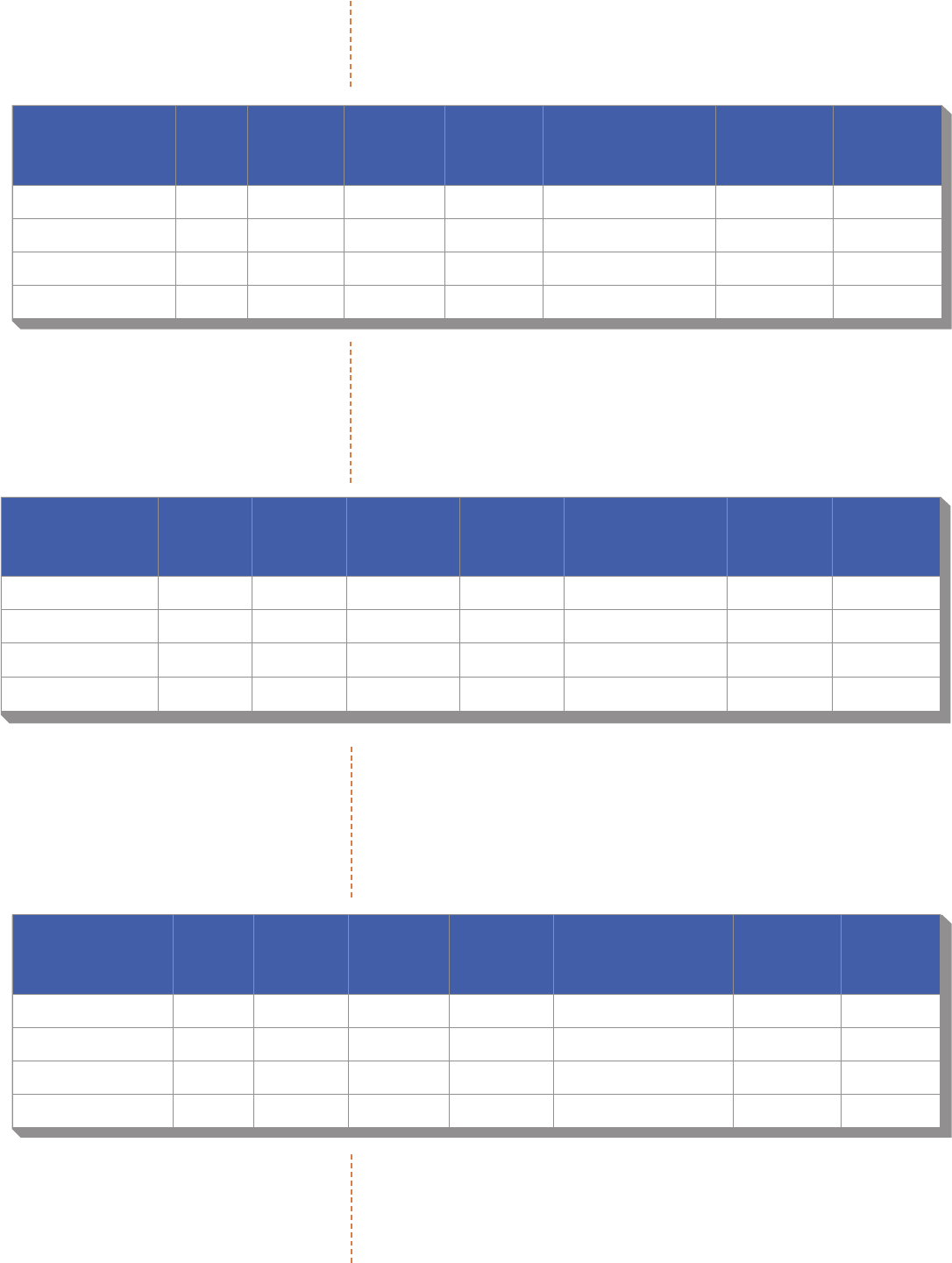

The ISO rates for these locations are listed in the table below.

They were provided by insurance carrier representatives

contacted for this study and were modied by the loss

conversion factor stated above.

Since the other important variable in determining total

insurance cost is the value of the building to be insured, we

researched typical building costs using historic, published

RS Means data for each of the six building types in the four

locations. The following table shows the building costs

produced by this research.

Final gross insurance costs for each location can be then

calculated by multiplying the insurance rate by the building

cost divided by 100. The chart below shows the theoretical

annual cost for insurance for each building. This cost is for re

and multi-peril (re, windstorm, earthquake) insurance on the

building only and does not include insurance on the contents in

the building. So what does the data show?

The above table shows that the cost to insure our model

building is less than either frame or joisted masonry in all four

states. It also shows that metal buildings cost less to insure than

any class of building in California. If insurance cost is the only

Location Frame

Joisted

Masonry

Metal

Building

System 1

Metal

Building

System 2

Masonry

Noncombustible

Modied

Fire-

Resistive

Fire-

Resistive

Bryan, TX $0.42 $0.39 $0.33 $0.27 $0.25 $0.14 $0.14

Delray Beach, FL $0.88 $0.86 $0.84 $0.47 $0.46 $0.37 $0.34

DuBois, PA $0.21 $0.18 $0.15 $0.13 $0.12 $0.07 $0.07

La Mesa, CA $0.17 $0.19 $0.10 $0.09 $0.16 $0.12 $0.12

Location Frame

Joisted

Masonry

Metal

Building

System 1

Metal

Building

System 2

Masonry

Noncombustible

Modied

Fire-

Resistive

Fire-

Resistive

Bryan, TX $692,000 $713,000 $756,524 $756,524 $720,500 $764,000 $993,200

Delray Beach, FL $765,500 $783,000 $834,741 $834,741 $800,000 $837,500 $1,088,750

DuBois, PA

$860,500 $875,000 $972,625 $972,625 $893,500 $937,500 $1,218,750

La Mesa, CA

$970,500 $952,000 $1,016,900 $1,016,900 $935,000 $1,016,600 $1,321,580

Location Frame

Joisted

Masonry

Metal

Building

System 1

Metal

Building

System 2

Masonry

Noncombustible

Modied

Fire-

Resistive

Fire-

Resistive

Bryan, TX $2,895 $2,757 $2,522 $2,030 $1,783 $1,098 $1,362

Delray Beach, FL $6,736 $6,708 $7,012 $3,909 $3,653 $3,127 $3,720

DuBois, PA $1,764 $1,531 $1,475 $1,281 $1,028 $672 $873

La Mesa, CA $1,682 $1,793 $1,017 $932 $1,480 $1,220 $1,586

The cost to

insure a metal

building is

signicantly lower

than frame and

joisted masonry

buildings...

factor in a decision regarding building type, metal buildings

would win out over frame and joisted masonry and would

be competitive with all types in California. Metal buildings

are reasonably competitive with Masonry Noncombustible

buildings in all four states.

While annual insurance costs for metal buildings are

signicantly higher than re-resistive buildings, the cost to build

re-resistive buildings typically runs about $200,000 more than

a similar metal building; so it would take many years to recoup

the difference in annual insurance cost for the building owner.

The data also shows that the cost to insure a metal building is

signicantly lower than frame and joisted masonry buildings

while the cost of construction for a metal building is only

slightly higher than the construction cost of both frame and

joisted masonry structures. The higher cost of construction can

be recouped by the building owner of a metal building in a few

short years just from a lower insurance cost on the building.

While insurance cost may be a competitive factor in building

construction decisions, it is only one of several factors that

affect the nal decision. If insurance cost is a major factor in the

decision for the owner, make sure the owner is getting accurate

cost gures from the carrier or agent handling the insurance

and not from the contractor offering a competitive alternative

to a metal building. When authorized by the potential owner,

speak with the owner’s insurance agent to make sure the agent

is familiar with the construction details of the proposed metal

building.

Objections to higher insurance cost for a metal building can

be overcome by looking at initial price, but also other factors

such as maintenance costs, speed of construction, and ease of

future building changes. In some cases, the owner may wish

to consider adding a sprinkler system to a metal building. In

this instance, the insurance cost for the metal building would

be lower than a non-sprinklered re-resistive or modied

re-resistive building. Just considering the insurance cost,

sprinklering a metal building might make nancial sense if the

additional cost of the system is less than the cost differential

between building types. See Insurance Bulletin No. 10 for more

details.

When competing with a building construction type that may

have a lower initial cost than a metal building (such as a frame

building), lower insurance cost, as well as other quality aspects

of a metal building will need to be emphasized to help make

the sale!

© 2015 MBMA